This post was written by Makenzie Johnson, an undergraduate student majoring in gerontology and psychology.

What is long-term care?

Long-term care (LTC) is a type of help that people receive over long periods of time when they may be unable to live completely independently. It can take place in a nursing home, assisted living facility, or at home with home health care. Long-term care is not the same as, say, a short stay in a skilled nursing facility after a surgery or injury, but rather assistance for day-to-day care, such as bathing, feeding, and therapies.1

What is long-term care insurance?

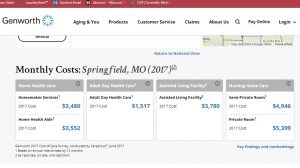

Long-term care is expensive when paying out-of-pocket and can create an even bigger dent in the budgets of older adults, which may already be limited. The average semi-private nursing home room in Springfield, Missouri costs just under $5,000 per month and can be expected to nearly double in the next twenty years.2 LTC is usually not covered under Medicare, which will only cover short-term stays in a nursing home during recovery or sometimes a short period of home health care under strict circumstances. While not for everyone, long-term care insurance can help cover the cost of this assistance. As with other types of insurance, individuals purchase a policy and pay a monthly premium, then their benefits kick in when they receive qualifying LTC. Each LTC insurance policy is different, so it is important to pay attention and closely compare the ones offered to you. Some may pay for care up to a certain dollar amount, while others may pay for a certain amount of time.1 Most LTC insurance policies won’t start paying until after an elimination period, which is a period of time that the individual needs care before benefits kick in. There may be other requirements as well, such as a certain level of impairment or limitation to activities of daily living before the individual can receive benefits.3

Some things to consider

- Your income: LTC insurance is not the best option for everyone. It is important to think about your current income and retirement savings. LTC insurance premiums in Missouri can range from $500 to over $4,000 each year for an individual, depending on the amount of coverage and how early you start paying in.5 If you cannot afford a premium now or don’t think you will be able to afford one in the future, it may not be a good idea to add a policy to your expenses, as you don’t want to waste all the money paid in over time if you decide to drop the policy later.1,3

- Your age and health: It may be cheaper to purchase a LTC insurance policy while you are young and healthy. Some policies have requirements that may prevent you from getting affordable coverage if you are older or have certain health conditions, so it’s good to start thinking about it now if you are younger.3

Some alternative options

- Medicaid: For those who qualify, Medicaid will pay for nursing home care or a limited amount of home health care. For those with a limited income who are eligible, this may be a better option for paying for LTC than LTC insurance.1

- Social support system: Friends and family members may be able to provide supportive care if they are geographically close enough to do so. This is considered informal support and is a low- or no-cost option.1,3

- Partnership Policy Plans: Partnership policies are a type of LTC insurance policy that may make it easier to qualify for Medicaid coverage once LTC insurance benefits have been exhausted by allowing for a certain amount of assets to be exempt from Medicaid eligibility guidelines. For every dollar that the insurance policy pays out, a dollar’s worth of the policyholder’s assets is ignored when determining that person’s eligibility.4 Individuals must still meet other eligibility requirements, however. The Medicaid benefits are the same, but the individual gets to keep a larger portion of his or her assets.

Around 70 percent of individuals aged 65 and up will require some form of long-term care. Each one is different, and there is no universally right way to pay for this care. What is important is that you plan for your future and the care that you may need. Consider your options and choose the one that is best for you and your loved ones.

References

- Education & Outreach. (2016, May). Understanding long term care insurance. Retrieved from https://www.aarp.org/health/health-insurance/info-06-2012/understanding-long-term-care-insurance.html

- Cost of care. (n.d.). Retrieved from https://www.genworth.com/aging-and-you/finances/cost-of-care.html

- Long-term care FAQs. (n.d.). Retrieved from https://insurance.mo.gov/consumers/LongTerm/FAQ.php

- Frequently asked questions for partnerships. (n.d.). Retrieved from https://insurance.mo.gov/consumers/LongTerm/FAQPartnership.php

- LTC insurance calculator. (n.d.). Retrieved from https://www.genworth.com/products/care-funding/long-term-care-insurance/ltc-insurance-calculator.html